Living in Houston means enjoying vibrant culture and economic opportunity, but it also means facing the unique weather challenges of the Gulf Coast. Your home is your most significant investment, and protecting it requires an insurance policy that understands the specific threats posed by our region-from hurricane-force winds and torrential flooding to intense hailstorms. Standard homeowners insurance often falls short, leaving Texas families vulnerable to catastrophic financial loss. This guide will walk you through the essential coverages, critical policy options, and proactive steps you can take to ensure your Houston home is fully protected against the realities of our environment.

Understanding Gulf Coast Home Insurance Risks

Houston's geographical location makes it a hotspot for a variety of severe weather events that directly impact property. The flat terrain and proximity to warm Gulf waters create a perfect storm scenario for hurricanes and tropical storms, which bring a triple threat of wind, rain, and storm surge. Unlike inland areas, Houston properties must be insured against these compounded perils. A standard HO-3 policy, the most common form of homeowners insurance, will typically cover wind damage but explicitly excludes flooding, which is a primary cause of loss during major storms like Hurricane Harvey.

Beyond hurricanes, Houston homeowners must contend with other frequent and damaging events. Severe thunderstorms can produce large hail that devastates roofs and siding, while the region's expansive clay soil is prone to shifting, leading to foundation issues. Furthermore, the high humidity can contribute to mold growth, which may not be covered if it's deemed a result of neglected maintenance or an excluded water event. Understanding that a one-size-fits-all policy is insufficient is the first step toward building a robust insurance safety net tailored to the Gulf Coast's demands.

Essential Insurance Coverages for Houston Homes

A comprehensive Houston homeowners insurance policy is built on a foundation of core coverages, each designed to protect a different aspect of your property and financial well-being. It is crucial to review your policy's declarations page to understand your limits and deductibles for each of these areas.

Dwelling and Other Structures Coverage

Dwelling coverage is the cornerstone of your policy, paying to repair or rebuild your house if it's damaged by a covered peril like fire, wind, or hail. Given Houston's construction costs and the potential for widespread damage after a major storm, you must ensure your dwelling coverage limit is high enough to completely rebuild your home at current market rates-this is known as replacement cost value, not its market or tax-appraised value. Other Structures coverage protects detached buildings on your property, such as a garage, fence, or shed, typically for 10% of your dwelling coverage limit.

Personal Property and Loss of Use

This coverage applies to the contents of your home-furniture, electronics, clothing, and other personal belongings. If a tornado or fire destroys your home, this coverage helps replace your possessions. For high-value items like jewelry or art, you may need scheduled personal property coverage with higher limits. Loss of Use coverage, also known as additional living expenses, is critically important after a major disaster. If your home is uninhabitable due to a covered loss, this coverage pays for temporary housing, restaurant meals, and other costs above your normal standard of living while your home is being repaired.

The Non-Negotiable: Flood Insurance

In Houston, purchasing a separate flood insurance policy is not a suggestion; it's a necessity. Many homeowners learned this difficult lesson during Hurricane Harvey, when widespread flooding damaged properties far outside designated high-risk flood zones. It is a common and costly misconception that homeowners insurance covers flood damage-it does not. Flood insurance is a separate policy, most often obtained through the National Flood Insurance Program (NFIP), though private flood insurance options are becoming more available in Texas.

When considering flood insurance, you must account for the two main types of coverage: building property and personal contents. The building property coverage insures the physical structure of your home, including its foundation, electrical and plumbing systems, and major appliances. Personal contents coverage protects your belongings inside the home. There are coverage limits with NFIP policies, so if you have a high-value home, you should discuss excess flood insurance with your agent to ensure full protection. Remember, there is typically a 30-day waiting period from the date of purchase before an NFIP policy goes into effect, so do not wait for a storm to be in the Gulf to buy coverage.

Special Considerations for Windstorms and Hurricanes

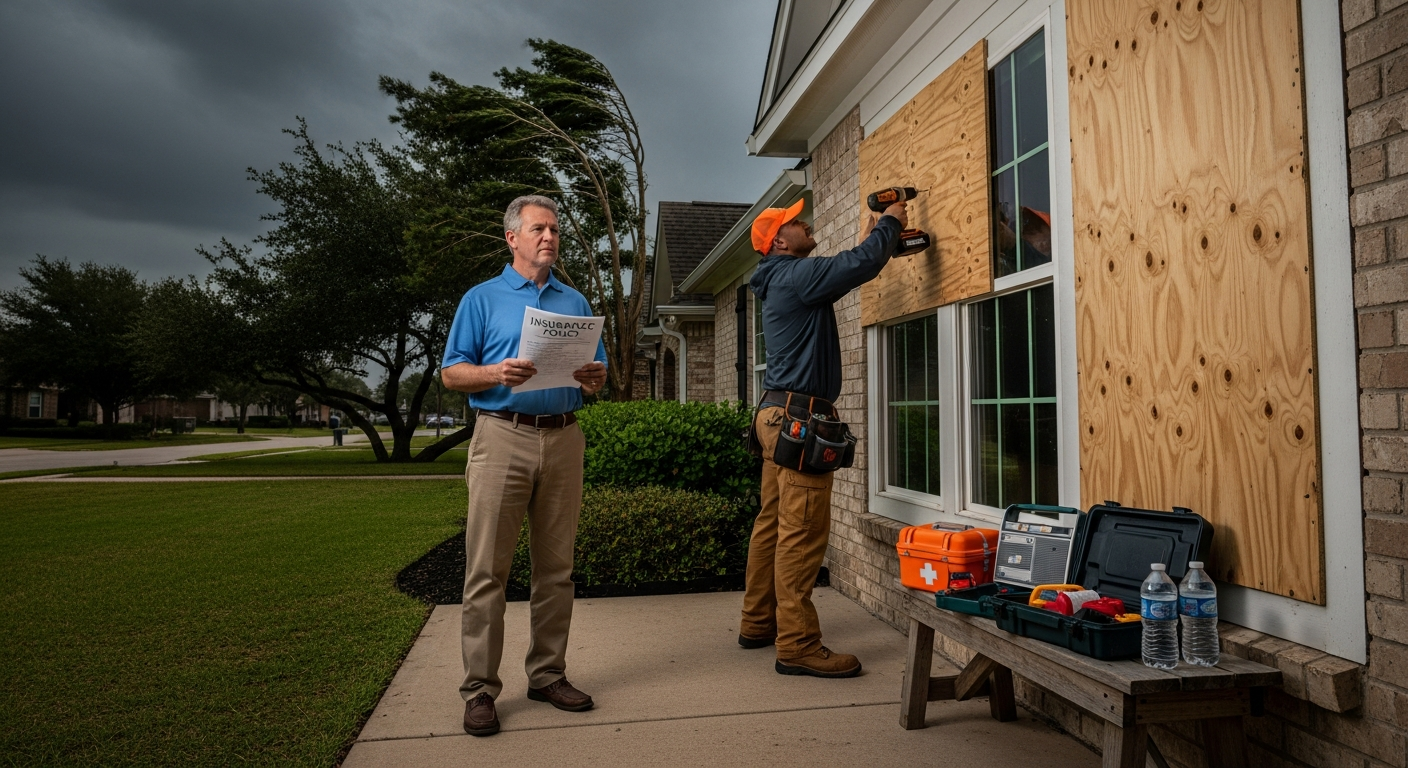

Wind damage is a primary concern for Gulf Coast residents, and Texas insurance policies handle it uniquely. Many insurers along the coast utilize a separate windstorm deductible, which is often a percentage of your dwelling coverage (e.g., 1-5%) rather than a standard flat dollar amount. This means if a hurricane damages your roof, your out-of-pocket cost could be significantly higher than for other types of claims. Furthermore, some companies may exclude wind damage entirely in certain coastal areas, requiring homeowners to seek coverage through the Texas Windstorm Insurance Association (TWIA).

TWIA is a residual insurance market that provides wind and hail coverage for property owners in designated coastal counties who are unable to find it in the private market. To be eligible for TWIA coverage, your property must meet specific windstorm construction requirements. It is vital to confirm whether your policy includes wind coverage, what your deductible is, and if you need a separate TWIA policy. Failing to do so could leave you responsible for the entire cost of repairing wind damage after a hurricane.

How to Choose the Right Houston Home Insurance Policy

Selecting the right policy involves more than just comparing premium costs. It requires a careful analysis of coverage details, deductibles, and the insurer's reputation for handling claims. Here is a step-by-step framework to guide your decision.

- Assess Your Replacement Cost: Work with your agent to conduct a detailed replacement cost estimate for your dwelling and personal property. Do not rely on square-footage calculators alone.

- Compare Deductibles: Scrutinize the deductibles for wind/hail, hurricane, and all-peril claims. Understand how a percentage deductible translates to actual dollars.

- Review Coverage Limits and Sub-Limits: Ensure the limits for other structures, personal property, and loss of use are adequate. Check for sub-limits on valuable items like jewelry or electronics.

- Verify Endorsements: Ask about valuable endorsements like guaranteed replacement cost, water backup coverage, and ordinance or law coverage, which pays for bringing your home up to current building codes during repairs.

- Check the Insurer's Financial Strength and Reviews: Choose a company with strong financial ratings (like A.M. Best) and positive customer feedback, especially regarding their claims process after major storms.

After you've narrowed down your options, have a final conversation with your insurance agent. A good agent at a Texas-focused agency will ask detailed questions about your home's construction, its location relative to floodplains, and the value of your assets to ensure there are no gaps in your protection. They can explain the nuances of how different policies would respond to a hypothetical hurricane or hailstorm, giving you confidence in your choice.

Practical Steps to Mitigate Risk and Lower Premiums

Proactive home maintenance and mitigation can not only protect your property but also lead to significant insurance discounts. Insurance companies reward homeowners who take steps to reduce the likelihood and severity of a claim.

Start by fortifying your home against wind and water. Installing storm shutters, reinforcing your roof with hurricane clips, and sealing openings can prevent wind from getting underneath and lifting your roof. To mitigate water damage, ensure your gutters are clean and that your yard is graded to direct water away from your foundation. Consider installing a battery-powered sump pump with a backup. For flood-specific discounts, you can have an elevation certificate prepared to show your home's lowest floor is above the Base Flood Elevation (BFE).

Beyond physical improvements, you can also lower your premiums by:

- Bundling Policies: Purchasing your auto and homeowners insurance from the same carrier often results in a multi-policy discount.

- Increasing Your Deductible: Opting for a higher deductible on your standard perils can lower your premium, but ensure you have the savings to cover that deductible if needed.

- Maintaining a Good Claims History: Avoiding small claims can help you maintain a claim-free discount.

- Installing Protective Devices: Smoke alarms, burglar alarms, and deadbolt locks can sometimes qualify for discounts.

Discuss these options with your insurance agent. They can provide a precise list of mitigation projects that their company recognizes with discounts and help you understand the return on investment for each upgrade.

Protecting your Houston home is an ongoing process that blends the right insurance policy with diligent maintenance and preparedness. By understanding the specific Gulf Coast risks, securing the essential coverages-especially flood insurance-and taking proactive steps to harden your property, you can transform your homeowners policy from a simple requirement into a powerful shield. Regularly review your coverage with a trusted local agent to ensure it evolves with your home's value and the ever-changing Texas climate, giving you the peace of mind that comes from true preparedness.